Energy Market Trends for Remainder of 2026 and Cascading Macro/Geopolitical Impacts

- Energy Market Fundamentals

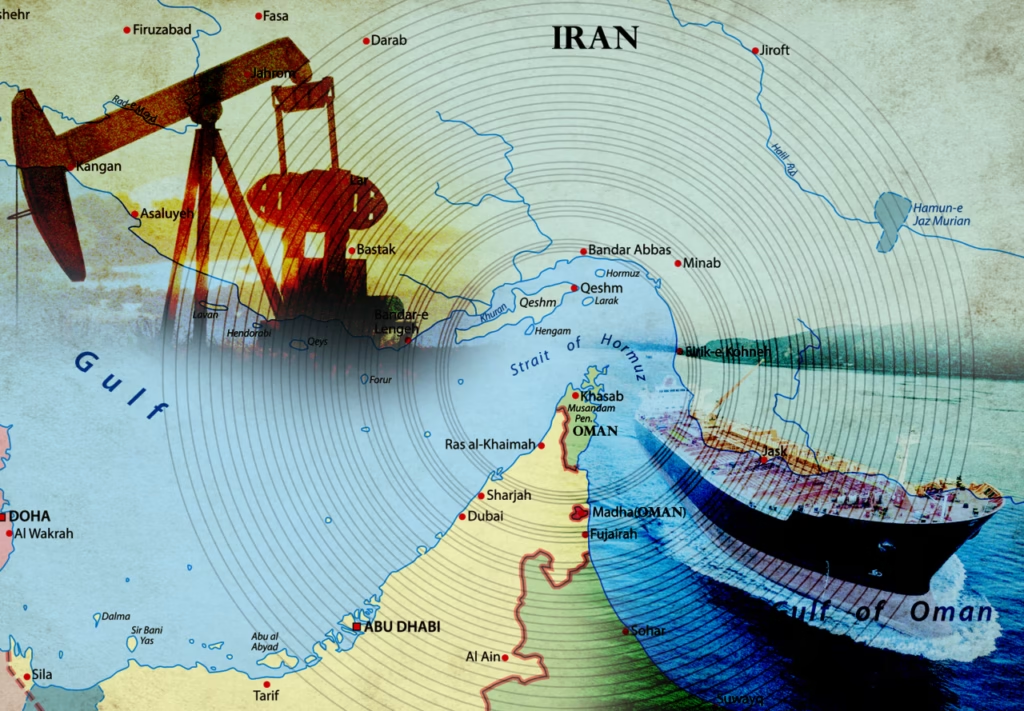

The current oil market is dominated by the largest supply disruption in history: the US-Israel strikes on the Islamic Republic (late Feb 2026) and ensuing near-blockade of the Strait of Hormuz (handling ~20 mb/d pre-conflict). Gulf producers (incl. OPEC+ members) have curtailed output by at least 10 mb/d, with crude production down ~8 mb/d in March alone per secondary sources and IEA data. Brent spiked near $120/bbl intraday before easing to ~$92–$110 range; WTI followed. OPEC+ responded with a modest +206 kb/d voluntary increase from April, but this is dwarfed by the outage scale.

Oil Company Dynamics: Major producers are capitalizing on the price spike while maintaining discipline. Saudi Aramco is rerouting limited volumes via Red Sea pipelines and has signaled potential buybacks; its low-cost structure positions it for outsized gains. U.S. supermajors (ExxonMobil, Chevron) and European peers (Shell, TotalEnergies) have minimal direct Hormuz exposure and are seeing windfall free cash flow—analysts project $60B+ extra industry-wide from sustained $90–$110 prices. Exxon and Chevron are accelerating U.S. shale (Permian) and Guyana (Stabroek block) output, with 2025 production already up 9–12% y-o-y and 2026 targets at 3.9–4.7% growth via acquisitions (e.g., Chevron-Hess) and efficiency. Strategies emphasize upstream focus, capex restraint, dividends, and buybacks; cash-flow neutrality for U.S. shale remains ~$47–$60/bbl. Force majeure declarations by some Gulf firms are creating short-term tightness, but majors are hedging via diversified portfolios.

Stock Market Dynamics: Energy equities have rotated sharply as a geopolitical and inflation hedge. The Energy Select Sector SPDR (XLE) is up 33–40% YTD/Q1 amid broader S&P 500 weakness (~–4–7%). Exxon, Chevron, and ConocoPhillips shares have gained 5–7%+ (or more in some sessions) since the spike, with record valuations for Shell and others adding over $130B in combined market value in the first two weeks post-conflict. However, the rally has been uneven—some names lag the outright price move due to temporary disruption risks and prior 2025 profit compression from softer averages. Sector breadth is strong, with upstream, midstream, and refiners all participating; RSI technicals show occasional oversold dips, but overall positioning reflects resilience and dividend appeal.

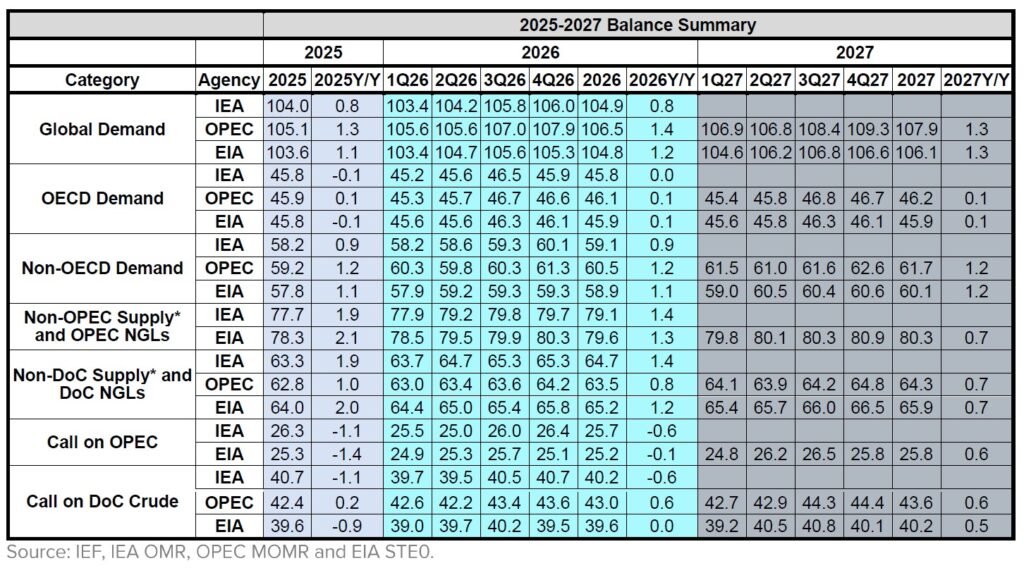

OPEC MOMR Holds firm on 2026 global demand growth at +1.4 mb/d y-o-y (OECD +0.15 mb/d; non-OECD +1.2 mb/d, led by India/China). DoC crude call unchanged at ~42.9 mb/d (0.6 mb/d above 2025). Non-DoC liquids supply (US/Brazil/Canada/Argentina) +0.6 mb/d. OPEC views the market as balanced once flows resume, emphasizing “supportive economic activities” and robust non-OECD transportation/industrial demand. Arabic coverage (e.g., Khaberni, Al-Estiklal) highlights record Gulf crude premiums (Oman/Kuwait) amid Hormuz risks but notes OPEC+ flexibility to avoid oversupply post-resolution.

IEA Oil Market Report (March 2026): More cautious. Revises 2026 demand growth down sharply to +640 kb/d y-o-y (–210 kb/d from prior), citing conflict-driven curbs (~1 mb/d hit in Mar–Apr from jet fuel/LPG/shipping). Global supply still +1.1 mb/d overall (all from non-OPEC+), but March saw –8 mb/d plunge. Stocks at historic 8.2 billion barrels (Jan data) provide buffer; IEA coordinated 400 mb emergency release from members. French sources (Les Echos, Boursorama, Challenges) frame this as “plus grande perturbation de l’histoire” with Gulf output slashed (e.g., –12 mb/d regional estimate from Kpler).

EIA STEO (March 2026): Brent forecast >$95/bbl near-term (Q2 risk premium), then <$80 Q3 and ~$70 end-2026 (assuming partial resolution). US production rises to 13.6 mb/d in 2026. Pre-conflict bearish views (JPM Feb: ~$60/bbl average on surpluses; Reuters poll ~$61 Brent) have been overridden by geopolitics.

JPM’s Natasha Kaneva (Global Commodities Strategy) previously stressed “soft fundamentals” and surpluses requiring cuts for $60 stabilization; post-spike, she notes temporary misalignment but reversion to fundamentals. Dr. Mamdouh G. Salameh-type views (OilPrice echoes) flag $100–$150+ spikes in full closure but expect $70–$80 reversion. French analysts tie +$40/bbl to –0.1 pp GDP (INSEE). Consensus: H2 2026 downward pressure post-resolution ($60–$85 base), asymmetric upside from chokepoint risks.

- Macroeconomic Transmission (Harper’s Quantitative Modeling)

Oil shocks transmit via cost-push (transport/fertilizers/chemicals ~40–60% of CPI weights in major economies) and demand-pull slowdowns (real income erosion). US resilience via shale/domestic buffers contrasts with Europe/Asia net-importer vulnerability. Harper’s cross-model synthesis (OECD interim, S&P, SocGen/Barclays quantifications, adjusted for current $90–$110 spot):

- Dollar value: USD strengthens as safe-haven/oil invoicing asset; DXY historically +2–4% on sustained $20+ spikes. Importers hoard dollars.

- Tariff wars: Secondary amplifier (US-China flows already fragmented); energy dominates near-term inflation. No direct offset to oil-driven pressures.

- Inflation/Stagflation: +0.5–2.0 pp global headline (energy-weighted); growth drag –0.1 to –1.0 pp. Europe/Japan sharper hits.

Risk-Weighted Scenarios (Remainder 2026; 60/25/15 probabilities calibrated to IEA/EIA/OECD/OPEC divergence + conflict duration):

Scenario (Prob.) | Brent H2 Avg. | Global GDP Δ (vs. ~3.3% baseline) | Global Inflation Δ | USD Index | Stagflation Risk (High if >0.5pp drag + >1pp inflation) | Key Driver |

Base Resolution (60%) | $75–$85/bbl | –0.1 to –0.3 pp | +0.5 to +0.8 pp | Modest ↑ | Low–Moderate (US cushioned) | Hormuz partial reopen + OPEC+ management + 400 mb SPR buffer |

Prolonged Disruption (25%) | $100–$120+/bbl | –0.5 to –1.0 pp | +1.0 to +2.0 pp | Strong ↑ | High (Europe/Asia acute; US relative winner) | Extended blockade/mining; limited bypass capacity |

Swift De-escalation + Cuts (15%) | $60–$70/bbl | +0.2 to +0.4 pp | –0.3 to –0.6 pp | Neutral/↓ | Negligible | Rapid flows resume + voluntary restraint |

These align with Harper’s sensitivity: every sustained $10/bbl adds ~0.2–0.3 pp inflation / –0.1 pp GDP globally (OECD-weighted). US PCE peaks ~3.8% Q2 if short shock; Europe faces sharper industrial/affordability squeeze. No stagflation baseline—US shale caps domestic pass-through.

- Geopolitical & Political Landscape Impacts (Lucas’s Power-Dynamics Analysis)

Sustained elevated prices ($80–$110 range) tilt relative power toward major producers/exporters. US (net exporter, 13.6 mb/d output) gains leverage: energy security buffers tariff negotiations, SPR draws, and ally support demands (e.g., tanker insurance/strait security). Russia benefits from revenue windfalls sustaining operations; China absorbs import costs but retains diplomatic cards. Europe (import-dependent) faces compounded vulnerabilities—second energy crisis echoes—accelerating LNG diversification but exposing competitiveness gaps.

Broader Landscape: US producer strength reinforces strategic autonomy without ideological overlay. OPEC+ cohesion tested but flexible (voluntary adjustments). Commentators (Kaneva: historical regime-change spikes +76%; IEA: “duration of Hormuz disruptions” decisive) underscore temporary volatility over permanent realignment—fundamentals reassert post-resolution.

Sources (key; full tool-traced):

- OPEC MOMR (Mar/Apr 2026 releases).

- IEA Oil Market Report – March 2026.

- EIA Short-Term Energy Outlook (Mar 2026).

- JPMorgan (Natasha Kaneva).

- Arabic: Al Jazeera, Arabic Trader, Khaberni.

- French: Les Echos, Boursorama, Challenges (INSEE ties).

- German: FAZ/SWP consistent framing.

- Macro/Political: OECD, S&P, Brookings, Politico, Reuters.